Why Intermittent Energy Is Permanently Dirty Energy

There is a claim so often repeated in energy policy that it has acquired the weight of scripture: renewables complement nuclear and fossil fuels — they do not compete with them. Building solar and wind is costless in strategic terms, a pure addition to a nation's energy portfolio with no trade-offs worth mentioning. "It doesn't hurt to have them," goes the refrain. "Every megawatt of solar is a megawatt of coal we don't burn."

This is wrong. In a world of finite capital, finite engineers, finite copper, finite concrete, and rising demand, every resource allocated to intermittent generation is a resource not allocated to firm, dispatchable power. The cost of renewables is not measured only in dollars per megawatt-hour. It is measured in what you did not build instead — and in what you will never become as a result.

We can prove this with arithmetic. Not ideology, not preference, not political affiliation. Just arithmetic.

I. ENERGY IS PROSPERITY

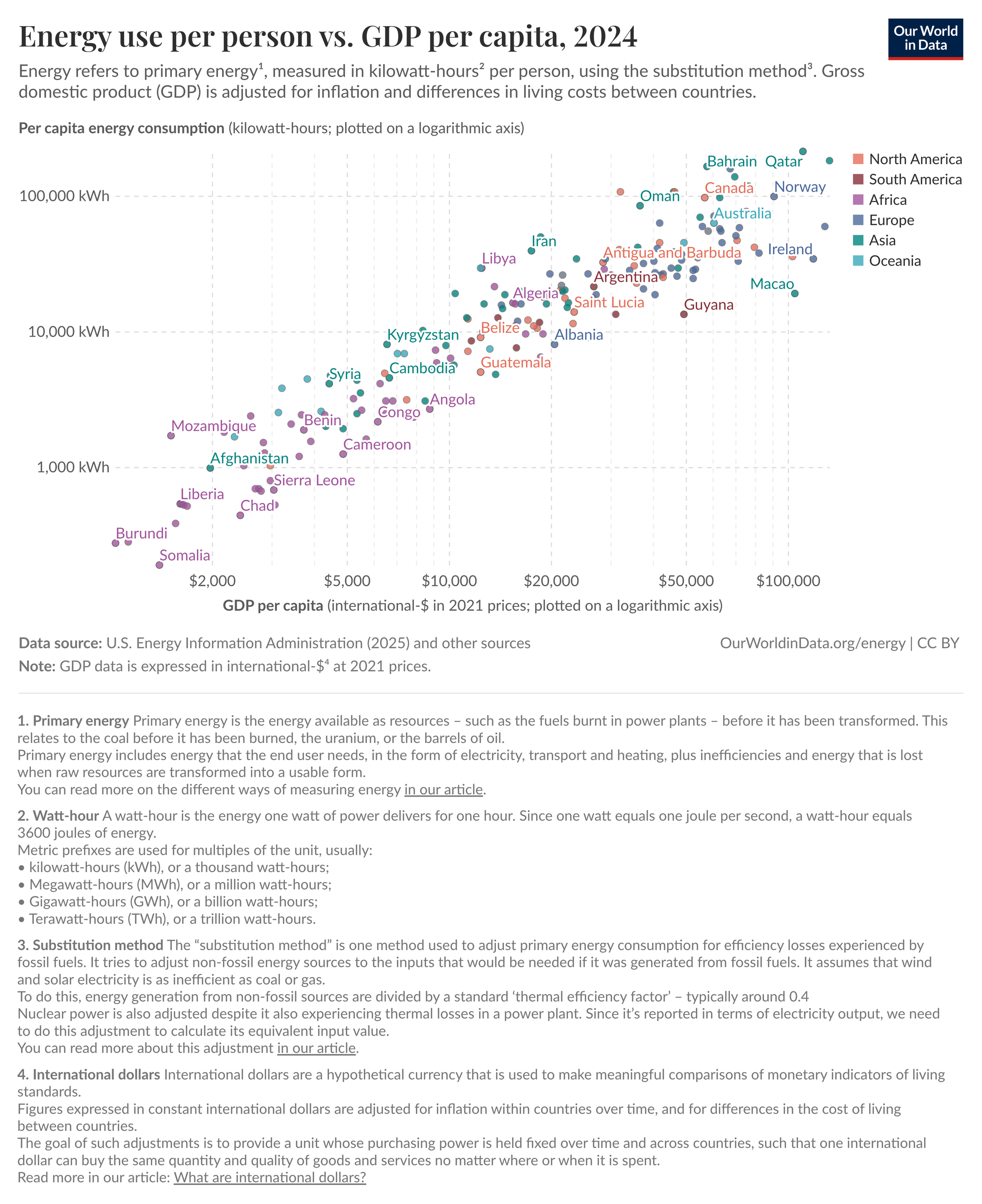

Plot GDP per capita against energy consumption per capita across all nations and the relationship is stubbornly, almost perfectly linear. Qatar, Norway, the United States, and Australia cluster at the top right. Bangladesh, Ethiopia, and Myanmar at the bottom left. There are virtually no rich, low-energy countries. The gap is not closing: EU nominal GDP per capita stood at roughly $40,000 in 2024, versus over $85,000 in the United States — a gap of more than 50% that has widened, not narrowed, over the past two decades. Even on a purchasing-power-adjusted basis, the deficit is 38%. The apparent exceptions — Switzerland, Ireland — are either running on hydro geography they did not choose or have GDP figures inflated by corporate tax structures that do not reflect real domestic production.

The popular narrative of "decoupling" — that advanced economies grow GDP while reducing energy use — dissolves under scrutiny. When Germany reports declining energy intensity, a significant share of that decline is offshoring. The smelter moved to Guangdong. The aluminium still gets produced. The energy still gets consumed. It simply no longer appears on the importing nation's books.

Getting richer requires more energy per person. This is not policy. It is physics. And every forty years or so, a step-change in demand arrives: electrification, petrochemical suburbia, digital infrastructure, and now AI compute and data centres — with demand projected to rise 160% by 2030. The nations that match each wave with firm energy get richer. The nations that miss it stagnate. A nation that builds the wrong energy infrastructure for the coming wave locks itself out of the economic future the grid is supposed to power.

II. THE NON-NEGOTIABLE GRID

Before the cost spreadsheets come out, before anyone mentions carbon credits, there is a prior question that renewable advocates never answer honestly: can civilisation function on intermittent power?

No. Not "no, but we're working on it." Not "no, but batteries will solve it." A categorical, engineering-level no.

Your refrigerator does not negotiate with the wind. Hospital ventilators do not check the weather forecast. The servers routing bank transactions, air traffic control systems, water treatment plants, the cold chain keeping food safe from farm to supermarket — all require power that is there when needed, not when the sun decides to shine.

Imagine a grid built entirely on renewables. A week-long high-pressure system settles over northern Europe in January — cold, still, dark. The Germans call it Dunkelflaute: the dark doldrums. Wind collapses. Solar produces almost nothing through winter cloud. Hospitals switch to diesel generators — burning fossil fuel to survive the clean grid. Smelters face catastrophic equipment damage. Heat pumps fail in millions of homes whose gas boilers were removed by government mandate. Food spoils. Traffic systems go dark. Not because of war, but because the wind did not blow for ten days.

III. THE ARITHMETIC OF IMPOSSIBILITY

No serious grid operator proposes solving this with batteries. Published plans from European grid bodies rely on interconnection, flexible gas turbines, and eventually green hydrogen. But it is worth running the battery math as a thought experiment, because the impossibility of the numbers reveals why every proposed solution to intermittency ends up requiring fossil fuel or nuclear somewhere in the chain.

On a peak winter day, Germany's grid consumes roughly 1.5 terawatt-hours of electricity, with the daily average closer to 1.3. A severe ten-day Dunkelflaute — rare but documented, with events of eight to twelve days in historical records — would require on the order of thirteen to fifteen terawatt-hours of stored energy. The entire planet's combined battery deployment in a given year, across all electric vehicles, phones, laptops, and grid storage, is in the range of two to three terawatt-hours. Germany alone would need several years of total global battery production just for its own winter backup.

In hardware terms, using the industry-standard Tesla Megapack at 3.9 megawatt-hours per shipping-container-sized unit, Germany would need 3.8 million of them. Packed with necessary clearance for cooling, inverters, and maintenance access, this battery farm would cover roughly 150 square kilometres — about the size of Miami.

The materials are worse. Using standard nickel-manganese-cobalt battery chemistry, the array would require roughly 2.25 million tonnes of refined cobalt. The Congo, which produces approximately 76% of the world's cobalt, mined about 220,000 tonnes in 2024. It would take over a decade of that country's entire output — shipping to nobody else on earth — just to build the cathodes. Alternative chemistries avoid cobalt but run into equally severe lithium constraints, requiring multiples of the entire African continent's known reserves.

At optimistic prices of $130 per kilowatt-hour, even the lower end of the storage range costs $1.7 trillion. The upper end approaches $2 trillion. That is the batteries alone, excluding land, copper cabling, inverters, substations, and labour. And lithium-ion batteries degrade. They must be completely replaced every fifteen to twenty years.

The materials do not exist in those quantities. The manufacturing capacity does not exist. And even if all of it materialised overnight, you would need to repeat the entire exercise every two decades. A fleet of nuclear plants, occupying a tiny fraction of the land and consuming a tiny fraction of the materials, runs for sixty years, requires no backup, and eliminates the need for any of it.

At this point, the sophisticated advocate abandons batteries and pivots to the real solutions: grid interconnection, green hydrogen, and demand response. These are the technologies that serious grid planners rely on. They also prove the thesis of this essay. Interconnection means that when the wind dies in northern Germany, you import electricity from France — from French nuclear reactors. This is not renewables solving intermittency. It is nuclear solving intermittency, delivered via a cable that crosses a border. Green hydrogen produced from surplus renewable electricity requires three to four units of electricity input for every unit of usable energy output — a thermodynamic penalty that turns an already expensive system into a ruinously expensive one, and that only works during the surplus hours, which are precisely the hours when the electricity was already unwanted. And demand response — the idea that industry will simply reduce consumption when the weather is unfavourable — is a euphemism for telling factories to shut down when the wind drops. It is the medieval energy model repackaged in management consultancy language: production halts when nature dictates. None of these solutions eliminate the need for firm power. They defer it, redistribute it, or disguise it. Follow every proposed solution to intermittency to its logical end and you will find, at the bottom of the chain, either a gas turbine or a nuclear reactor. The question is whether you build the reactor deliberately, or back into the gas turbine by accident.

IV. THE OVERPRODUCTION ADVANTAGE

At this point, the renewable advocate retreats to a more sophisticated position: renewables handle variable demand — the peaks, the daytime surges — while nuclear provides baseload. They work together.

This is fatally flawed, because demand peaks on cold, dark winter evenings — precisely when solar output is zero and wind, despite higher winter averages, is subject to prolonged collapses during blocking events. It is not the seasonal average that matters but the variance. Meanwhile, solar floods the grid on summer afternoons when demand is moderate — Germany now records negative wholesale prices six to nine percent of all hours, paying neighbours to take unwanted power. You have built capacity that produces most when you need it least.

The renewable advocate will now reach for the most popular number in energy economics: the Levelised Cost of Energy. LCOE for solar and onshore wind is indeed at historic lows — in many markets, the cheapest electricity ever generated. This is true, and completely beside the point. LCOE measures the cost of generation alone. It excludes the gas plant that must be built to cover nights and windless days. It excludes the grid reinforcement required to connect remote wind farms to urban load centres. It excludes curtailment — the electricity produced at times nobody wants it, which in Germany is now paid to be disposed of. It excludes capacity payments to keep gas turbines on standby. It excludes the balancing costs of frequency regulation on a grid with volatile input. It is the equivalent of quoting the price of a car engine without the chassis, the wheels, or the fuel system, and claiming you have the cheapest car on the market. When you add the full system cost — backup, grid, curtailment, balancing, capacity payments — the delivered cost of a reliable megawatt-hour from a renewable-heavy system is two to four times the LCOE alone. And the irony is that the electricity produced at LCOE's cheapest moments is worth the least, because supply peaks precisely when demand is moderate. The cheapest electricity ever generated, and generators pay to give it away. This is not a market success. It is a market failure with a favourable press agent.

Nuclear overproduction solves this, and it is not theoretical. France built the bulk of its 56 reactors in under two decades, runs them around the clock, and exports the surplus — the largest net electricity exporter in Europe, sending roughly 50 to 90 terawatt-hours per year to its neighbours depending on conditions. Nuclear generates approximately 70% of French electricity. Carbon intensity: fifty to sixty grams per kilowatt-hour, about six times lower than Germany's 371. Industrial electricity prices consistently below the European average. No fleet of gas peakers needed to survive winter. Overproduction is not waste. It is cheap surplus — exportable, convertible to hydrogen, or simply offered to consumers at prices that stimulate growth. The marginal cost of running a reactor at 95% instead of 85% is nearly zero. Germany chose the opposite path. It built the most expensive electricity system in Europe, backed it with the dirtiest fuels in Western Europe, and now imports French nuclear power to keep its grid alive in winter.

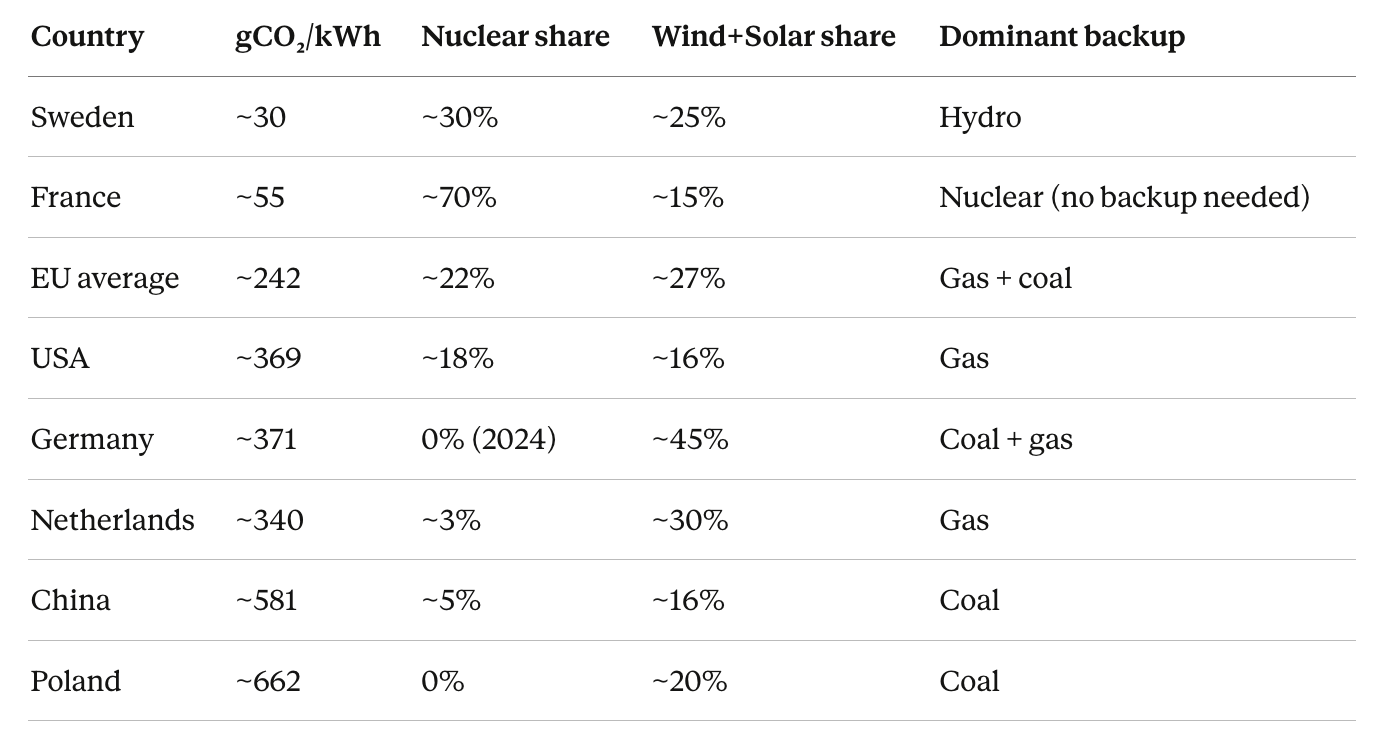

The table tells the story that no amount of policy language can disguise. Grid carbon intensity, measured in grams of CO₂ emitted per kilowatt-hour of electricity generated (2023–2024 data, Ember / IEA):

Read the table vertically. The cleanest grids are nuclear grids. The dirtiest grids include some of the highest renewable penetrations on earth. Germany has 45% wind and solar — more than France, more than Sweden, more than the United States — and emits nearly seven times more CO₂ per kilowatt-hour than France. The Netherlands has 30% wind and solar and emits six times more than France. This is not transitory. It is not a phase that will be solved by adding more panels. It is structural and permanent, because when the wind drops, the gas turbine fires — and it will fire every winter, every Dunkelflaute, every cold still evening, for as long as the grid depends on intermittent sources. A country that is 45% renewable is also, by definition, 55% fossil on the hours that matter. You cannot average your way out of a winter.

The advocate's answer — interconnection will solve this, by importing clean power from neighbours when renewables fail — is already failing. The EU's own regulator, ACER, reports that 1,700 gigawatts of renewable projects are stuck in grid connection queues across Europe — more than six times Germany's total installed capacity. The legally mandated target requiring 70% of cross-border transmission capacity to be available for trade by the end of 2025 was missed by most member states. In practice, many TSOs made only 30 to 50% of physical capacity available. Grid congestion cost €4.3 billion in 2024 alone. Seventy-two terawatt-hours of mainly renewable electricity were curtailed that year — roughly equivalent to Austria's entire annual consumption, thrown away because the grid could not absorb it. Negative price hours surged from 154 in 2018 to over 1,000 by late 2024. And in April 2025, the Iberian Peninsula experienced a cascading grid failure that left millions in Spain and Portugal without power for sixteen hours — a real-world demonstration of what happens when an interconnected but fragile system loses its balance. Dublin and Amsterdam have paused new data centre projects entirely, citing grid unavailability. Wait times for grid connection in the EU now range from two to ten years. This is not a system that is being built. It is a system that is failing to be built — and it is failing in real time, with real consequences, documented by the EU's own agencies.

And yet the persistent answer from Brussels is always the same: more integration. More interconnection. More Europe. The reality behind the rhetoric is the opposite. France has systematically obstructed cross-border interconnection with Spain for decades. Spain's environment minister publicly stated that it is "very hard to make progress with them in terms of energy interconnections." Two planned interconnector projects through the Pyrenees — Navarra-Landes and Aragón-Atlantic Pyrenees — were originally scheduled for 2030. They have been delayed to 2036 and 2041 respectively. A €3 billion undersea cable through the Bay of Biscay faces activist blockades in the Landes. As of 2025, Spain still had not met the EU's 10% interconnection target — a target that was set for 2020. France has no commercial incentive to build these links. It is Europe's largest electricity exporter. Its nuclear fleet produces some of the cheapest electrons on the continent. Why would it build cables that would allow Spanish solar to undercut its export prices?

And here is the final absurdity of the "integrated European market" that is supposed to make renewables work. The EU's wholesale electricity pricing system is based on marginal cost — the price of the last, most expensive megawatt-hour needed to meet demand in any given hour. In most European markets, that marginal unit is a gas turbine. This means that even when 70% of the electricity in a given hour comes from nuclear or renewables — produced at near-zero marginal cost — the wholesale price is set by the gas plant that produced the final 5%. France, which generates the cheapest electricity in continental Europe, is forced to sell at the price set by Germany's gas peakers. French consumers pay gas-indexed prices for nuclear power. French industry competes against American industry that pays the actual cost of its generation. The system punishes the country that built the best infrastructure and rewards the country that built the worst — all in the name of "market integration." Every time a European politician calls for more integration as the solution to the energy crisis, they are calling for more of the mechanism that is transferring French nuclear surplus value to German gas plant operators. This is not a market. It is a subsidy from the competent to the incompetent, enforced by treaty.

It is worth noting how France achieved this. The Messmer Plan of 1974 was not submitted to public referendum. It was not debated on television panels or workshopped through citizen assemblies. It was an executive decision, taken by technocrats who understood the physics, imposed by a president who had the institutional power to act on what the arithmetic demanded. There was protest. There was opposition. The plants were built anyway. Forty years later, France has the cheapest and cleanest electricity in continental Europe.

This is not an argument against democracy. The United States thrives precisely because its executive has the constitutional authority to set direction — Trump's nuclear executive orders, whatever one thinks of them politically, demonstrate that a president can pivot national energy strategy in a single term. Switzerland, with its direct democracy, holds referendums on specific technical questions and lets citizens decide with remarkable sophistication. Both systems produce decisive outcomes because they concentrate choice: one person decides, or everyone decides. Both work.

What does not work is the European model of coalition governance — the system that dominates Germany, Belgium, the Netherlands, Italy, and increasingly the European Union itself. Coalition politics does not produce decisions. It produces compromises. And compromise in energy policy does not mean finding the optimal path between two reasonable positions. It means a Green party demanding the closure of nuclear plants as the price of entering government, a liberal party insisting on market mechanisms that never materialise, and a conservative party quietly protecting coal jobs in swing regions. The result is policy that nobody designed, nobody believes in, and nobody would have chosen if given the option. It is the two-metre giraffe: technically assembled from the right parts, but built to the wrong specifications and dead on arrival.

Italy banned nuclear by referendum after Chernobyl — then again after Fukushima, an event 9,000 kilometres away in a seismic zone with no analogue in the Mediterranean. Austria voted the same way. Germany's phase-out was the price the Social Democrats paid for a coalition with the Greens. In each case, the system produced the answer that was politically easiest, not the answer that was correct. And in each case, the consequence is identical: higher emissions, higher costs, deeper dependence on fossil fuels and on neighbours who made better decisions.

Walk down any shopping street in Brussels or Berlin. Turn on the television. Listen to the conversation at dinner. How many people in that room can explain what a gigawatt-hour is? How many understand why their electricity bill doubled, or can articulate the relationship between energy density and purchasing power? Almost none. These are not failures of intelligence. They are the ordinary limits of specialisation in a complex society. No one votes on bridge load tolerances or aircraft wing geometry. Energy infrastructure is no less technical and no less consequential. But European coalition politics has made it a bargaining chip between parties rather than an engineering problem solved by engineers.

A fair objection deserves a fair answer. Yes — a solar panel on a roof, when the sun is shining, displaces some generation that would otherwise come from a reactor or a gas turbine. In a system where every kilowatt-hour matters, that displacement has marginal value. But this is precisely the point: in a system with sufficient nuclear capacity, the displacement is worthless. France already produces more electricity than it consumes. It exports the surplus. If you have built enough reactors to cover peak demand with margin, the solar panel on the roof is not displacing fossil fuel. It is displacing nuclear output that was already clean — and the reactor keeps running anyway because you cannot economically ramp it down for a few sunny hours. The panel has produced nothing that the grid needed. It has merely shifted clean electrons from one source to another at vastly greater capital cost.

And that capital cost is the real crime. A European household that spends €15,000 on rooftop solar — subsidised by the state, financed by debt — has locked that capital into an asset that produces intermittent power worth a few hundred euros per year, degrading over time, requiring inverter replacement within a decade. That same €15,000, invested in equity markets, in startups, in venture funds, in the companies building the next wave of industrial technology, would compound and create real wealth — the kind that funds pensions, employs engineers, and deepens capital markets. Multiply this by millions of households across Europe and you begin to see the scale of the misallocation. Tens of billions of euros in household savings, redirected from productive investment into rooftop hardware that the grid does not need, producing power the grid cannot use at the hours it arrives, backed by subsidies the state cannot afford.

This is why European capital markets remain shallow compared to the American system. Capital that should be flowing into innovation — into the deep, liquid, risk-taking markets that produced Google, Tesla, Nvidia, and every frontier AI company — is instead sitting on rooftops in the form of silicon panels, earning a regulated feed-in tariff, producing no compounding return, creating no jobs, funding no research. The United States has deep capital markets because American savings flow into equities, venture capital, and productive assets. Europe has shallow capital markets because European savings flow into government bonds, property, and subsidised hardware. The solar panel is not just a bad energy investment. It is a bad investment, full stop — and every euro it absorbs is a euro that will never fund the European Nvidia that does not exist and, at this rate, never will.

And the solar panel is only the beginning. The European Union's Energy Performance of Buildings Directive requires member states to enforce minimum energy ratings on residential property. Homes must be retrofitted to meet Category A or B standards — new insulation, heat pumps, triple glazing, ventilation systems — or face restrictions on sale or rental. The cost falls entirely on households. A typical deep retrofit in France, Belgium, or Germany runs €30,000 to €60,000 per dwelling. There are roughly 220 million residential buildings in the EU. Even a partial programme — retrofitting only the worst-performing stock — implies hundreds of billions in private expenditure, spent by families who have already been taxed at 45 to 55% of gross income, who have already paid VAT on every purchase, who have already seen their energy bills double, and who are now being told to spend what little remains on insulation mandated by regulators who do not live in the houses, do not pay the bills, and do not bear the risk.

This is not investment. Investment produces a return. A homeowner who spends €40,000 on an energy retrofit in a country with declining property values, a weakening currency, and stagnant wages has not invested. They have complied. The money is gone. It will not compound. It will not fund a startup. It will not deepen a capital market. It will sit inside a wall, producing a marginally lower heating bill, in a house that is worth less than it was five years ago, in an economy that is producing less than it did a decade ago.

And for tens of millions of European dwellings, the mandate is not just expensive — it is physically impossible. The Haussmann apartments that define Paris. The canal houses of Amsterdam. The tiled façades of Lisbon. The medieval centres of Bruges, Prague, and Florence. These buildings cannot be retrofitted to Category A without destroying what makes them valuable. You cannot wrap a seventeenth-century limestone façade in external insulation. You cannot install triple glazing in a listed window frame. You cannot bore ventilation ducts through walls that are classified as national heritage. And you cannot demolish them, because they are the reason tourists come — and tourism is increasingly the only industry these cities have left. The directive demands that Europe's oldest buildings meet standards designed for new construction, in cities whose economies depend on those buildings remaining exactly as they are. It is regulation written by people who have never held a trowel, imposed on people who cannot afford a contractor, applied to buildings that cannot physically comply, in cities whose survival depends on non-compliance.

The American household, unburdened by any equivalent mandate, puts that same money into a 401(k), an index fund, a brokerage account — and it compounds at 8 to 10% per year for decades. Over thirty years, the difference between €40,000 buried in wall insulation and €40,000 invested in the S&P 500 is roughly €400,000. Multiply that by tens of millions of European households and you begin to understand why American household wealth dwarfs European household wealth — and why it always will, for as long as Europe forces its citizens to pour hard-earned, post-tax savings into unproductive mandated hardware while Americans pour theirs into productive financial assets.

V. THE GREEN PARADOX

It must be said plainly: arguing that renewables are wasteful for industrialised grids is not an anti-environmental position. It is, in fact, the most pro-environmental position available.

Being genuinely green is not about installing solar panels. It is about recycling, better materials, insulating buildings, circular supply chains. And every one of those things is energy-intensive. Recycling aluminium requires remelting at 660 degrees. Electric arc furnaces for recycled steel consume enormous electricity. Water purification, waste processing, advanced agriculture — all need cheap, abundant, reliable power. European industrial electricity costs average over $190 per megawatt-hour. American industrial electricity costs roughly $48 per megawatt-hour. Every green industrial process — every recycling plant, every insulation factory, every electric arc furnace — is four times more expensive to operate in Europe than in the United States. By choosing the most expensive electricity system — expensive in total system cost, including backup, curtailment, and grid reinforcement — renewable-committed countries raise the price of every green industrial process downstream. When electricity costs four times as much, recycling moves offshore and the circular economy becomes a PowerPoint presentation rather than a business. The country that abandoned nuclear in the name of environmentalism now burns more fossil fuel per kilowatt-hour than the country that kept it.

And then there is the electric vehicle delusion — perhaps the purest example of Europe's talent for mistaking symbolism for substance. A German or Dutch driver buys an electric car and believes they are saving the planet. But where does the electricity come from? In Germany, 39% of generation is still fossil — gas plants and coal plants that fire up every time the wind drops. In the Netherlands, gas generates roughly half of all electricity. When that driver plugs in on a cold, still evening, the marginal electron charging the battery comes from a gas turbine. This is the equivalent of buying a diesel generator, installing it in your garden, running a cable to your car, and calling yourself green. Nobody would do that. It would be absurd. But when the diesel generator is thirty kilometres away in an industrial park, connected by a wire you cannot see, the absurdity becomes invisible. Out of sight, out of mind. The emissions have not disappeared. They have been relocated — from the tailpipe to the smokestack, from the driver's conscience to the grid operator's balance sheet. In France, where nuclear provides 70% of electricity, an electric car is genuinely clean. In Germany, it is a fossil fuel vehicle with extra steps.

VI. THE OPPORTUNITY EUROPE ABANDONED

The waste is not only in steel, concrete, and land. It is in attention. Every nation has a finite number of nuclear engineers, grid planners, permitting officers, and research scientists. Every year those people spend on wind farm applications, solar grid interconnection studies, and battery subsidy programmes is a year they do not spend advancing fission.

The numbers are damning. In 1975, nuclear technologies received 73% of public energy research budgets across the industrialised world. By 2015, that share had collapsed to 20%, as governments redirected funding toward renewables and efficiency. The cumulative bill is staggering: the International Energy Agency projects $4.7 trillion in renewable subsidies over the period 2016 to 2040. In the United States alone, the Inflation Reduction Act committed $421 billion to wind and solar between 2025 and 2034. Annual global subsidies tell the same story in miniature: renewables receive roughly $128 billion per year; nuclear receives $21 billion — a six-to-one ratio in favour of the technology that requires permanent fossil backup over the technology that eliminates it. And what does that ratio buy? Nuclear generates approximately 10% of the world's electricity on 3% of global energy subsidies. Renewables, despite receiving 20% of subsidies, still cannot operate without firm backup. Every subsidy dollar spent on nuclear displaces more fossil fuel, more reliably, than every subsidy dollar spent on wind or solar.

The talent follows the money — in the wrong direction. The global renewable energy workforce reached 16.2 million in 2023. Solar alone absorbed over half a million new workers that year. These are not unskilled labourers. They are electrical engineers, materials scientists, grid modellers, civil engineers, project managers with advanced degrees — the exact same talent pool that builds reactors, designs containment systems, and advances fission research. Every one of them working on a wind farm interconnection study is one not working on next-generation reactor design. Every permitting officer processing a solar application is one not processing a nuclear licence. The renewable industry has become a giant siphon, draining the finite pool of technical talent into infrastructure that will always require fossil backup, and away from the infrastructure that would eliminate it. The opportunity cost is not hypothetical. It is 16.2 million people building redundant systems. China noticed. Its private nuclear research spending tripled between 2015 and 2020, reaching $1.3 billion annually. Chinese firms now hold seven of the top twenty-two positions in global nuclear industry research rankings. Global nuclear investment has risen 50% in the past five years, projected to reach $75 billion in 2025 — but almost all of that growth is in Asia and North America, not in Europe.

This matters because nuclear energy is the very technology that made postwar Europe rich. France's reactor fleet gave it energy independence, cheap industrial power, and an export surplus. Britain's early nuclear programme powered its postwar industrial recovery. Belgium, Sweden, Switzerland — each built prosperity on firm, dense electricity. Europe did not become wealthy selling olive oil and artisanal goods. It became wealthy because it had the cheapest energy on the continent and the engineering culture to exploit it.

Now that engineering culture is being dismantled. The number of students graduating with nuclear engineering degrees in the United States fell 25% between 2012 and 2022 — and that is the country now trying to rebuild. In the United Kingdom, 20% of the nuclear workforce is over 55. The European Nuclear Society estimates the continent will need over 300,000 new nuclear workers in the next fifteen years just to replace retirees and manage existing commitments — a pipeline that does not exist. Meanwhile, the United States is planning to grow its nuclear workforce from 68,000 to over 200,000 to meet its tripling targets. The civil servants who once processed nuclear permits in Europe are now processing wind farm applications. The institutional knowledge that built Gravelines and Ringhals and Doel is retiring and not being replaced.

Europe is not transitioning from nuclear to renewables. It is transitioning from an industrial economy to a service economy — and eventually to a tourist economy. The numbers confirm it: EU industrial production has declined 6% since 2022. In 2024 alone, it fell another 2%, with capital goods production dropping 7.5%. Automotive and transport equipment manufacturing shrank 6.4%. Since 2000, EU industrial output has grown at a cumulative average of just 0.6% per year — one-third the American rate and one-ninth of China's. Italy, once a manufacturing powerhouse, has recorded negative industrial production growth every year on average for a quarter of a century. The factories are becoming hotels. The research labs are becoming museums. The engineering schools are becoming business schools. This is not a transition. It is a controlled descent, dressed up in the language of progress.

VII. THE NUCLEAR QUESTION

Chernobyl was a Soviet reactor with no containment structure, operated during an unauthorised test by technicians who disabled multiple safety systems, in a political system without accountability. No modern design shares its fundamental flaw. Fukushima was a 1960s-era reactor struck by the fourth-largest earthquake in recorded history and a fourteen-metre tsunami. Confirmed deaths from radiation: one. Deaths from the evacuation itself: over two thousand.

There is no free lunch. Nuclear requires uranium mining — but a fuel pellet the size of a fingertip holds the energy of a tonne of coal. Solar requires open-pit mining for quartz, silver, and tellurium. Wind turbines require rare earth metals from mines whose tailings lakes are visible from space. The roughly 440 reactors worldwide have accumulated over 19,000 reactor-years of experience with a civilian death toll lower than annual coal mining fatalities in a single country.

And yes — new nuclear construction in the West is currently broken. Vogtle in the United States cost $35 billion, more than double its estimate. Flamanville in France is a decade late. Hinkley Point C in Britain is billions over budget. This essay does not pretend otherwise. But the cost of Vogtle, amortised over the sixty to eighty years those two reactors will operate, produces firm electricity at a lower system cost than renewables plus backup over the same period. The construction overrun is a one-time failure of project management. The gas plant backing up the wind farm runs forever. And the cost of not building nuclear — measured in decades of industrial decline, permanently higher energy prices, locked-in emissions, and lost economic output — dwarfs any construction overrun. France and South Korea proved that nuclear can be built on time and on budget. The answer to Western construction failures is not to default to an inferior technology. It is to fix the construction problem.

Humans cannot live without impact. The question is which footprint to choose. For off-grid communities in remote regions — a village in sub-Saharan Africa, a relay station in the Andes — distributed renewables are transformative. But a solution designed for 500 people off-grid does not scale to 84 million on-grid. That is not a complement. It is a category error.

VIII. THE THOUGHT EXPERIMENT EUROPEANS REFUSE TO RUN

Imagine that tomorrow morning, a laboratory in the United States announces commercially viable fusion. Energy costs drop by a factor of ten. Electricity becomes so cheap it is barely worth metering.

Would Europe refuse to adopt it? Declare that fusion is unnecessary because the continent has already invested in wind farms? Of course not. To refuse would be to accept poverty within a decade. Automation powered by near-free energy — Tesla deploying humanoid robots at scale, Jeff Bezos raising $100 billion through Project Prometheus to acquire and automate entire manufacturing sectors, American and Chinese factories running lights-out operations around the clock — would price European industry out of every global market within years. The continent would become what it quietly fears it is already becoming: a museum with good restaurants. Beautiful, cultured, and poor.

And yet that is precisely what Europe is doing right now — not with fusion, but with fission. The technology exists. It is proven. France demonstrated it forty years ago. It delivers energy at a fraction of the system cost of renewables. And Europe, as a matter of deliberate policy, has chosen not to use it. Germany shut its last reactors in 2023. Belgium is phasing out. Italy banned nuclear by referendum. The logic is identical to refusing fusion.

Prosperity is not a birthright. It is a function of productivity, and productivity is a function of energy. Decline is not announced. It arrives in the ordinary way — through prices that rise, factories that close, young people who leave, and a standard of living that erodes so slowly that each year feels normal until you look back and realise the country you grew up in no longer exists.

IX. THE SCOREBOARD

In 2000, European hourly labour productivity was roughly at par with the United States. By 2023, the gap had widened to ten percent for Germany, fourteen for France, twenty-eight for Italy. Seventy-two percent of the transatlantic gap in output per capita is now attributable to productivity differences. European industrial electricity prices in 2025 averaged over twice American levels and nearly fifty percent above China's. The EU's total value of sold industrial production fell from nearly six trillion euros in 2023 to 5.86 trillion in 2024 — a contraction in an economy that desperately needs growth. Chemical plants are closing across Germany. The United States operates roughly 5,000 data centres to Europe's 1,200.

The euro traded comfortably around 1.35 to 1.45 against the dollar before the sovereign debt crisis. It broke below parity in September 2022 for the first time in twenty years. As of early April 2026 it sits around 1.15 — roughly twenty percent below its pre-crisis average, with the risk of a sustained move back toward parity in the next twelve months entirely plausible. That is not a cyclical fluctuation. It is a market verdict.

The United States, for all its dysfunction, is pivoting. Executive orders target 400 gigawatts of nuclear by 2050. An eighty-billion-dollar partnership with Westinghouse launched for fleet-scale deployment. Tax credits for wind and solar expire mid-2026. And here is the point about step-change demand that the renewable model cannot answer: every major technology company on earth — the firms with the best capital allocation discipline in history, spending $480 billion on AI infrastructure in 2026 alone — has independently concluded that their future requires nuclear. Microsoft signed a twenty-year, $16 billion agreement with Constellation to restart Three Mile Island's 835-megawatt reactor. Amazon invested $650 million in a data centre next to Susquehanna's nuclear plant and backed 5 gigawatts of X-energy SMRs. Google signed the first corporate SMR fleet deal with Kairos Power for 500 megawatts. Meta announced 6.6 gigawatts of nuclear procurement. Oracle is building a gigawatt-scale data centre powered by three small modular reactors. These are not ideological decisions. These are capital allocation decisions made by the most ruthless optimisers of return on investment in the world. They looked at wind. They looked at solar. They chose nuclear — because a data centre that goes dark when the wind drops is not a data centre. It is a liability.

No renewable source can meet this demand. Not because the panels are too few, but because the physics is wrong. AI training runs take weeks of continuous, maximum-power computation. A single large language model training run consumes as much electricity as a small city — continuously, around the clock, for months. You cannot pause training when a cloud passes overhead. You cannot resume when the wind picks up. The next step-change in energy demand — AI, robotics, industrial automation, electrification of transport and heating — requires firm power, available on demand, every hour of every day. Renewables cannot provide this. They never will. The step-up belongs to nuclear. And every nation that does not build it will import the products of nations that did.

This is the deepest delusion in European energy policy: the targets are calculated against yesterday's demand. When Brussels announces that Europe will reach 42.5% renewable energy by 2030 — or, in the electricity sector, roughly 69% — those percentages are measured against current consumption. The consumption of an economy that is already deindustrialising, that has no hyperscale AI infrastructure, that has offshored its heavy manufacturing, and that has not yet begun to electrify its transport or heating at scale. And the 42.5% target covers total energy — but wind and solar only produce electricity, which is barely a quarter of total energy demand. The rest — transport, industrial heat, buildings — still runs overwhelmingly on oil and gas. The target sounds ambitious. It is measured against the smallest slice of the pie, in an economy that is shrinking. It is the energy equivalent of Louis XVI commissioning two hundred windmills in 1780 because that is what France's flour mills require — while across the Channel, the Industrial Revolution is about to multiply energy demand by a factor of a hundred. The windmills would have been sufficient for the France that existed. They would have been irrelevant to the France that was coming. Europe is making the same mistake today. It is planning its energy system for an economy that is contracting, not for the economy it would need to compete. The renewable target is not ambitious. It is an admission that Europe has given up on the industries that would require firm power — and on the step-change in total energy demand that would make even 69% renewable electricity look like a rounding error.

While America's most valuable companies are signing twenty-year nuclear contracts, Europe's most valuable industrial companies are leaving. The European Commission — unelected, unaccountable, and staffed overwhelmingly by career administrators — has systematically dismantled the continent's industrial base through regulatory overreach. REACH, the EU's chemical regulation framework, has contributed to 17.2 million tonnes of chemical production capacity being shut down across Europe since 2022. BASF, the world's largest chemical company, closed 11 plants at its Ludwigshafen complex in 2023, cut 2,600 jobs, and is investing €10 billion in a new production complex in Zhanjiang, China — effectively relocating its future from Germany to a country with cheaper energy and fewer regulators. Evonik cut 2,000 jobs. More than 200 German industrial plants face closure or scale-back.

Huntsman Corporation — a global chemical company that had its European headquarters and R&D centre in Everberg, Belgium — closed both and moved the functions back to The Woodlands, Texas. Its CEO stated on an earnings call that "Europe's focus on deindustrialisation was going faster than anyone expected." The company closed additional plants in Moers and Deggendorf in Germany and King's Lynn in the UK, and now serves its remaining European customers from facilities in Florida and Louisiana. A $6 billion chemical company concluded that it is cheaper to manufacture in Texas and ship across the Atlantic than to produce in Belgium — the country where it was headquartered. That is not a trade decision. It is a verdict on the cost of European energy, regulation, and taxes combined.

Chemical production output in Germany remains 15% below 2018 levels. The EU's share of global chemical sales collapsed from 27% in 2004 to 13% in 2024. China's rose from 10% to 46% over the same period. Gas prices in Europe remain 3.3 times higher than in the United States. The European Chemical Industry Council's own verdict: "no signs of improvement yet in 2025." Germany's chemical association: "a turnaround is still out of the question."

The pattern is identical across every sector the Commission touches. Euro 7 emissions standards threaten to make affordable cars impossible to manufacture in Europe. Energy performance mandates require millions of homeowners to retrofit buildings they cannot afford to insulate, freezing housing markets. The taxonomy regulation tells investors which assets are "sustainable" — a classification decided by bureaucrats, not markets. And through it all, European companies — the ones that remain — listen. They comply. They fill in the forms. They attend the consultations. They hire the compliance officers. And they watch American competitors, unencumbered by any of it, build the future at one-sixth the energy cost. The West has largely lost its nuclear construction expertise, but the answer to that is not to default to an inferior technology. It is to fix the construction problem. France and South Korea proved it can be done.

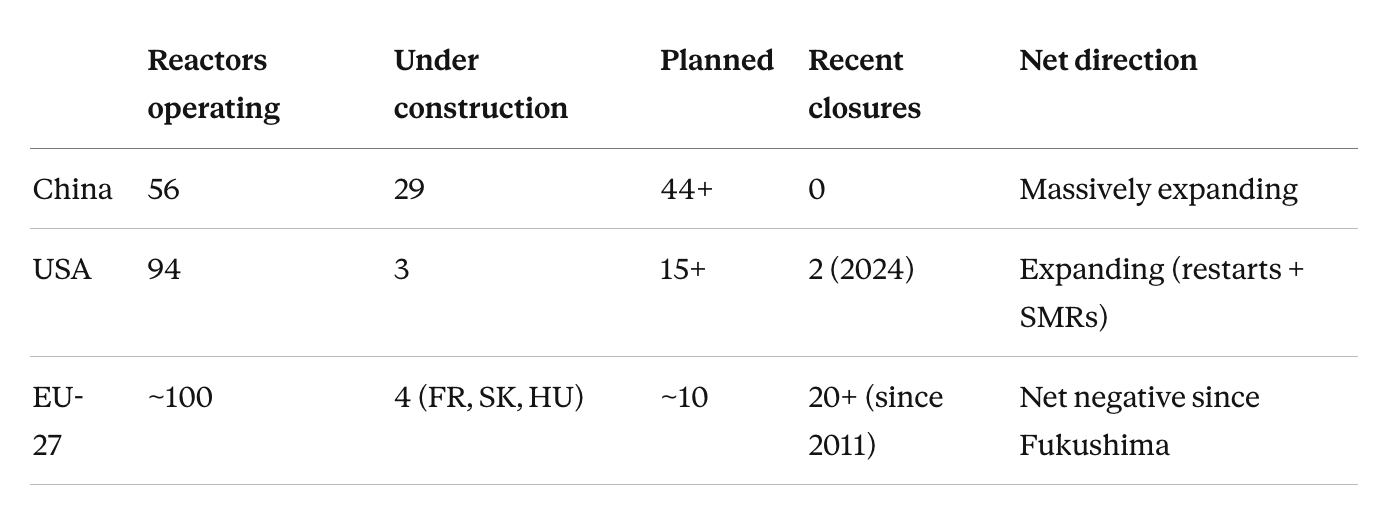

The nuclear pipeline makes the divergence concrete. As of early 2025, this is what the world's three major blocs are building:

Over the past five years, every single reactor construction start worldwide was carried out by either Chinese or Russian companies — without exception. Of the 40 construction starts in that period, 26 were in China, one in Pakistan by Chinese firms, and the remaining 13 by the Russian nuclear industry in Egypt, India, Turkey, and at home. No Western company started building a new reactor anywhere in the world in five years. Europe's sole reactor under construction by a European company — Flamanville 3 in France — took 17 years and cost €23.7 billion, seven times the original estimate. The French Court of Accounts described it as a catastrophe of project management. It finally connected to the grid in December 2024.

Meanwhile, China builds reactors in six years at one-third the cost, has already surpassed France in annual nuclear generation, and is on track to surpass the United States by 2030. The EU has closed more than twenty reactors since Fukushima — Germany's seventeen, Belgium's ongoing phase-out, Sweden's early closures — and added almost nothing. The pipeline tells you everything about where each continent will be in twenty years. China will have the world's largest nuclear fleet. The United States, if it executes its 400-gigawatt target, will have rebuilt its industrial base on firm power. Europe will have older reactors nearing end of life, no construction pipeline to replace them, and a grid that runs on imported gas when the wind drops. The euro will reflect this. It already does.

THE VERDICT

"It doesn't hurt to build renewables" is the energy equivalent of digging a second foundation next to the one you are already building. It consumes the same concrete, the same labour, the same time. And when you are done, you still only live in one house. Except you have spent twice as much, taken twice as long, and the house is colder than your neighbour's.

For off-grid communities in remote regions, renewables remain a lifeline. For the industrialised world, they are an expensive distraction from the only technology that matches the density of modern civilisation.

Europeans have travelled enough to know what a beautiful, poor country looks like. You have visited them. You admired the architecture, the food, the light. You tipped generously. You did not want to live there. You came home grateful for functioning infrastructure, reliable power, and an economy that could afford both. That is what decline looks like from the outside: charming. From the inside, it looks like your children leaving for New York, your factory closing, your pension shrinking, and your government explaining that progress was never really the point.

The countries that choose firm, dense, abundant energy will power the next century. The countries that do not will serve coffee to the ones that did.

FOR THOSE WHO STILL DON'T GET IT

Imagine two islands of cavemen, separated by open ocean, competing for survival.

The first island discovers a hot spring — a steady, reliable source of thermal energy, day and night, rain or shine. They use it to heat their shelters, cook food around the clock, fire crude pottery, and eventually smelt metal. They work in shifts. They build through the night. Their population grows because infants survive the winter. Within a few generations, they have tools, storage, surplus, and the beginnings of civilisation.

The second island builds a windmill. It works beautifully — when the wind blows. When it does not, they sit in the dark. They cannot smelt metal because the fire goes out mid-pour. They cannot store food reliably because the drying process requires continuous heat. They cannot work at night. They are, functionally, limited to the hours and seasons when the weather cooperates. Their progress is intermittent. Their surplus is unreliable. Their population grows more slowly because winter kills the vulnerable.

After a hundred years, the first island sends a boat to the second. They find a pleasant, quiet community — resourceful, clever, making the best of what they have. Living essentially as they always have.

What happens next is not pleasant. It is history. The first island, with its surplus of metal tools, preserved food, and manufactured goods, begins trading with the second. At first this looks like partnership. But the terms are set by the island that produces more, faster, cheaper. The second island has nothing to offer at comparable value. It sells raw materials — fish, timber, shells — at prices the first island dictates. Within a generation, the second island's economy is dependent on imports it cannot produce and exports it cannot price. Its skilled workers leave for the first island, where the forges pay better. Its young people learn the first island's language. This is not colonisation by force. It is colonisation by surplus. The island with firm energy does not need to conquer the other. It simply out-produces it until dependency is total and irreversible.

And if the second island resists — if it tries to impose tariffs on the first island's goods, or refuses to sell its timber at the offered price — the first island has a second option. It has metal. It has manufacturing. It has men who work through the night, fed by preserved food, armed with forged weapons. The second island has men who work when the wind blows. This is not a theoretical exercise. It is the history of every civilisation that fell behind in energy technology. The Romans did not conquer Gaul because they were braver. They conquered it because they had better logistics — roads, aqueducts, supply chains — all powered by firm, controllable energy in the form of grain surpluses and engineered infrastructure. The British did not build an empire because they were morally superior. They built it because coal gave them steel, steam, and the ability to project power across oceans while their competitors were still burning wood. Energy dominance is not a metaphor for geopolitical power. It is the mechanism.

Europe's choice to run on intermittent energy is not a charming lifestyle preference. It is planned serfdom — a voluntary surrender of the industrial capacity, the military capacity, and the economic independence that firm energy provides. The continent that once ruled the world because it mastered energy first is now choosing to be the second island: pleasant, quiet, resourceful, and completely dependent on the ones that did not make the same mistake.

This is the choice. It has always been the choice. The specific technologies change — hot springs become fission, windmills become solar panels — but the structure of the problem is permanent. A civilisation with firm energy advances continuously. A civilisation with intermittent energy advances intermittently. Over time, the gap between them becomes uncrossable.

Anyone who believes intermittent energy is "good enough" for an industrial economy is making a statement about the kind of civilisation they are willing to accept. They are saying: we do not need to operate at night. We do not need to run factories through the winter. We do not need continuous computation, continuous cold chains, continuous manufacturing. We can pause when the weather pauses. That is not a modern energy policy. It is a medieval one. And the people who advocate for it deserve to experience what medieval energy availability actually felt like — the cold, the dark, the idle hours, the dependency on seasons, the inability to store, to build, to compound progress across time. For roughly a thousand years, that was the human condition. We escaped it with firm energy. We will return to it without it.

THE CAPITAL MARKETS KNOW

You do not need to read this essay to understand the thesis. You can read two stock charts instead.

Constellation Energy, the largest nuclear generator in the United States, traded at $38 per share in January 2022. By October 2025, it reached $412 — a tenfold return in under four years. Its nuclear fleet runs at a 94.7% capacity factor. Revenue in 2025 was $25.5 billion. Microsoft, Google, and Meta are fighting to buy its electrons. The market has priced in a simple reality: firm, zero-carbon power is the most valuable commodity in the AI economy.

Ørsted, the world's largest offshore wind developer, has experienced the opposite trajectory. In 2023, the company wrote down $5.7 billion after cancelling two flagship US wind projects. In early 2025, it took another $1.7 billion impairment. In August 2025, its shares fell 30% in a single day — their largest drop in history — after a planned asset sale collapsed and the company was forced to raise $9 billion in emergency equity. S&P downgraded it to one notch above junk. The company suspended dividends for 2023 through 2025, cut 800 jobs, and exited markets in Norway, Spain, and Portugal. Its stock has lost roughly 75% of its value from its 2021 peak. The most visible renewable energy company on earth is being dismantled by the economics of the technology it pioneered.

These are not anomalies. They are the market's verdict on two business models: one that sells power on demand, and one that sells power when the weather permits.

And Ørsted is not the exception. It is the template. Siemens Energy lost 40% of its market value in 2023 on wind turbine warranty provisions. Vestas, the world's largest wind turbine manufacturer, posted years of consecutive losses before a fragile recovery. SunPower, once the largest American residential solar company, filed for bankruptcy in August 2024. The pattern repeats across the sector: massive capital deployed into assets that produce a commodity nobody can store, at times nobody wants to buy, backed by subsidies that can be withdrawn by the next government.

The ETFs tell the story without spin. The iShares Global Clean Energy fund — the largest renewable energy ETF in the world — lost money four years in a row: minus 24% in 2021, minus 5% in 2022, minus 20% in 2023, minus 26% in 2024. Its five-year annualised return is negative 9%. Since inception, it has delivered a compound annual return of 0.83% — effectively zero — with a maximum drawdown of 71%. Investors pulled $1.7 billion in net outflows over three years. The Invesco Solar ETF was worse: minus 25% in 2021, minus 5% in 2022, minus 27% in 2023, minus 38% in 2024. Its five-year annualised return is negative 14%. A European who put €10,000 into the solar ETF in January 2021 held roughly €3,000 by December 2024 — before the currency loss. Both ETFs bounced roughly 47% in 2025, largely on speculative rotation, but they remain far below their 2021 levels. A dead cat bounces. It does not come back to life.

For comparison: the S&P 500 returned plus 27% in 2021, minus 18% in 2022, plus 24% in 2023, plus 26% in 2024. Constellation Energy, the nuclear generator, went from $38 to $412. The market is not confused about which technology works.

This is not volatility. Volatility goes both ways. This is a structural value trap — an industry that cannot generate returns on capital because the underlying product is worth less than it costs to produce and deliver. Subsidies delay the reckoning but do not prevent it. When the American Inflation Reduction Act's wind and solar credits expired in 2026, the props came out and the economics were laid bare. The technology is not competitive. It never was. The subsidies were not a bridge to competitiveness. They were life support.

European retail investors — the pensioners, the savers, the sustainability-fund subscribers who were told renewables were the future — are being wiped out twice. First by the equity losses in companies and funds that cannot generate positive returns over any meaningful timeframe. Then by the slow erosion of the euro itself, as the continent's energy policy drains competitiveness and drives capital to jurisdictions that chose firm power. In real dollar terms, a European renewable investor has lost over 80% of their purchasing power since 2021. This is not a temporary setback. It is the structural consequence of investing in a technology that does not work at industrial scale, in a currency backed by an economy that has chosen not to.

The generational implication is not abstract. It is already visible. European industrial jobs are migrating to the United States and Asia. The engineers are following. The venture capital is following. What remains is services, tourism, agriculture, and the public sector. Europe's children will not design reactors or build AI systems. They will renovate farmhouses into bed-and-breakfasts, serve coffee to American tourists, and wonder why their grandparents' generation — which had the technology, the engineers, and the capital to choose differently — decided that the wind was enough.

The fiscal wall. In a functioning market, unprofitable technologies die. Capital moves to what works. Risk is borne by shareholders, and failure is absorbed through bankruptcy. This is how SunPower ended — wiped out by economics, as it should be. But in Europe, the state has decided to reanimate the dead cat with public money. The problem is that the state is broke. Euro area government debt stands at 88% of GDP and rising. France runs a deficit of 5.8% — nearly double the EU's own 3% limit — with debt at 113% of GDP and interest payments surging 15% in a single year. Italy carries 135%. Greece, 154%. Twelve EU member states are running deficits above the legal ceiling. European governments already spend 49.5% of GDP — nearly half of everything produced — on public expenditure. There is no margin left.

And yet these governments are subsidising an industry that has never, in aggregate, generated a positive return on invested capital. The $4.7 trillion in projected cumulative renewable subsidies through 2040 is not coming from surplus. It is coming from debt — borrowed against the future productivity of economies that are already declining. When bond markets eventually reprice that risk — and they will, because bond markets always do — the subsidies will stop. Not because governments choose to stop them, but because they can no longer afford them. And on that day, every renewable asset that depended on state support for its survival will be marked to its true economic value: a fraction of what was paid for it. The taxpayer will absorb the loss. The pensioner will absorb the loss. And the dead cat, despite a decade of public resuscitation, will remain exactly where it was.

The Germany counterfactual. A peer-reviewed study published in 2025 quantified what the nuclear shutdown actually cost. Without the phase-out, Germany would have avoided 230 million tonnes of CO₂ emissions, 5,800 deaths from air pollution, and nearly 56,000 cases of severe illness — all attributable to the additional coal and gas burned to replace nuclear output. The grid's carbon intensity would have been 48% lower. The share of electricity from fossil fuels in 2023 would have been 27% instead of the actual 47%. PricewaterhouseCoopers calculated that if Germany had simply kept its reactors running, 94% of its electricity generation in 2024 would have been emission-free. Instead, the actual figure was 61%.

These numbers will worsen, not improve. Germany is planning to build 20 gigawatts of new gas-fired power plants to backstop its renewable grid. As AI-driven electricity demand rises — estimates suggest an additional 50 to 100 terawatt-hours of demand in Europe by 2030 from data centres alone — those gas plants will run harder, not less. Germany shut down 17 reactors that generated 133 terawatt-hours of zero-carbon electricity per year. It is now building gas plants to fill the gap. The emissions trajectory is structurally locked in for decades.

The Chinese trap. There is a final irony that European policymakers appear incapable of seeing. The continent that lectures the world on green leadership believes it is following China's example. It is not. It is following China's export strategy — which is a very different thing.

Fossil fuels supply 86% of China's total primary energy. Coal alone accounts for 56%. In 2024, China added between 80 and 100 gigawatts of new coal-fired capacity — more than at any point in the previous nine years. It emitted 11.2 billion tonnes of carbon dioxide, roughly 31% of the global total and 4.5 times Europe's entire output. Wind and solar, despite the breathless headlines about installed capacity, deliver roughly 3% of China's total primary energy — once you count the full economy, not just the electricity grid. European commentators routinely confuse installed capacity with actual energy delivered, and electricity with primary energy. China has enormous solar and wind capacity on paper. It runs on coal.

But China manufactures 80% of the world's solar panels. It produces 70% of the world's wind turbines. It dominates the global supply chain for batteries, inverters, and rare earth processing. It is not building these products for its own energy security — it is building coal and nuclear for that. China currently has 29 nuclear reactors under construction — nearly half the global total — and plans to surpass the United States as the world's largest nuclear generator by 2030, building reactors in six years at one-third the cost of Western projects. It is building them for export.

The European policy establishment cannot see this because it has built an entire worldview around the opposite conclusion. The European Council on Foreign Relations calls China a "climate superpower" and a "renewable energy superpower" while noting, almost in passing, that coal generates 58% of its electricity. The EU Institute for Security Studies describes China as "cementing its position as the world's energy and industrial superpower" through renewables. Bruegel, the EU's most influential economic think tank, writes approvingly of China's "simultaneous expansion of renewables and coal" as a "deliberate policy approach." European commentators describe American energy policy as "sabotage" and "tearing up environmental standards" — referring to the country that is building $80 billion in new nuclear capacity, restarting retired reactors, and whose tech giants are signing twenty-year nuclear power agreements to fuel the AI economy.

The framing is consistent and pervasive: China is the responsible green leader. America is the reckless fossil polluter. The data says the opposite. China emits 4.5 times Europe's CO₂. The United States is building the nuclear fleet that will power the next industrial revolution.

The advocate will counter: but China is also deploying renewables domestically at record scale. This is true — and irrelevant to the argument. China is deploying everything at record scale. Coal, nuclear, hydro, wind, solar, batteries — all simultaneously, all at volumes that dwarf any other country. The difference is that China has the baseload already. Coal generates 55% of its electricity. Nuclear is expanding faster than anywhere else on earth. Renewables are deployed on top of firm power, as a supplement — reducing marginal coal burn during favourable weather while the baseload carries the economy through every hour of every day. Europe is attempting the opposite: building the supplement without the foundation, and hoping the weather cooperates. China adds renewables because it can afford to. Europe adds renewables because it cannot afford nuclear — having spent thirty years dismantling the workforce, the permits, and the political will required to build it.

European technocrats have internalised a narrative manufactured in Beijing and repeated in Brussels — and they are making trillion-euro investment decisions based on it. They are not following China's energy model. They are buying China's products with borrowed money, calling it leadership, and wondering why the factories keep closing.

The fastest road away from oil runs through nuclear. This is the point most renewable advocates miss entirely. The argument for nuclear is not merely about electricity. It is about replacing oil and gas across the entire economy. With abundant, cheap nuclear electricity, you can electrify heating — France already runs millions of homes on nuclear-powered heat pumps and electric radiators, at a fraction of the carbon cost of German gas boilers. You can produce green hydrogen at scale for industrial processes, steelmaking, and heavy transport, using nuclear heat and electricity around the clock rather than waiting for sunny afternoons. You can power electric vehicle fleets with firm electrons rather than intermittent ones backed by gas. You can desalinate water. You can run direct air capture. Every pathway to eliminating fossil fuels from transport, industry, and buildings requires electrification — and electrification requires electricity that is always on.

Nuclear overproduction makes oil redundant faster than any other technology on earth. France has already demonstrated this: its per-capita oil consumption is lower than Germany's, its heating sector is more electrified, and its transport sector is catching up. The country that kept nuclear is decarbonising faster across all sectors — not just electricity — than the country that chose renewables. The renewable grid cannot replace oil because it cannot reliably power the systems that would replace oil. The nuclear grid can. And does.

WHY WE WRITE THIS

Every euro of debt raised to subsidise renewable energy passes nothing to the next generation except the obligation to repay it. Not a reactor that will run for sixty years. Not a competitive industrial base. Not cheap electricity. Just debt — serviced by an economy that is shrinking, in a currency that is weakening, against competitors who chose differently. This is not investment. Investment generates returns. This is consumption of future wealth to fund present symbolism.

Wonder why not a single European company leads in artificial intelligence. Not one. Not in large language models, not in AI chips, not in cloud infrastructure, not in autonomous systems, not in humanoid robotics. The reason is not cultural. It is not a lack of talent — Europe produces excellent engineers and mathematicians. The reason is energy. AI research requires massive, continuous compute. Compute requires massive, continuous electricity. European industrial electricity costs six times the American level. That ratio does not produce a competitive disadvantage. It produces an impossibility. You cannot train a frontier model when every GPU-hour costs six times what your competitor pays. You cannot build a hyperscale data centre when the grid operator tells you there is a two-year wait for a connection and no guarantee of firm supply. You cannot attract AI investment when the marginal cost of electricity is set by a gas peaker that fires every time the wind drops. Europe's energy policy has not merely slowed its AI ambitions. It has killed them. The continent that invented the World Wide Web, built CERN, and produced some of the finest scientific minds in history cannot compete in the defining technology of the twenty-first century — because it decided that wind turbines were more important than reactors.

This is not just an energy failure. It is an innovation failure, a productivity failure, and ultimately a civilisational failure. Cheap energy is the substrate on which everything else grows: industrial innovation, scientific research, manufacturing competitiveness, startup formation, creative risk-taking. When you price energy at six times your competitor, you do not get six times less innovation. You get no innovation — because the innovators leave. They go to Austin, to San Francisco, to Singapore, to anywhere the lights stay on and the power is cheap. What remains is heritage tourism, artisanal production, and the public sector.

Benchmark follows arithmetic to its conclusions. The investment implications are stark. The United States is repositioning toward energy abundance at exactly the moment AI and reshoring demand it. The $80 billion nuclear partnership, the hyperscaler power agreements, the regulatory streamlining — these are structural bets on firm power that underpin dollar strength and the continued outperformance of American assets.

For European investors, the hedge is straightforward: hold dollar-denominated assets in companies building the infrastructure of the next century. The euro against the dollar is a real-time scoreboard of two continents' energy decisions. It has been in structural decline for nearly two decades and the fundamentals are worsening, not improving.

And if you need a physical metaphor for what European decline looks like in practice, consider this: a château in the Loire Valley — six bedrooms, formal gardens, outbuildings, centuries of history — sells for €200,000. A comparable property in Connecticut or Virginia commands $10 million or more. The exchange rate between those two numbers is not a curiosity. It is the market's answer to the question of which civilisation is producing value and which is consuming its inheritance.

Wait a few more years. The castles will be cheaper still. The factories that once paid for them will be hotels. And the debt raised to build wind farms that required gas plants that required coal plants that required imports from France — that debt will still be there, compounding quietly, passed to children who will wonder what their grandparents were thinking.

The countries that choose firm, dense, abundant energy will power the next century. The countries that do not will serve coffee to the ones that did. The arithmetic is not complicated. It never was.

Disclaimer

Please note that Benchmark does not produce investment advice in any form. Our articles are not research reports and are not intended to serve as the basis for any investment decision. All investments involve risk and the past performance of a security or financial product does not guarantee future returns. Investors have to conduct their own research before conducting any transaction. There is always the risk of losing parts or all of your money when you invest in securities or other financial products.

Credits

Photo by Raphael Cruz / Unsplash.