We have been cautious on U.S.-valuations since these reached new heights at the start of the year. After a sell-off, most growth stocks regained some steam. Where could this go?

1/ Inflation expectations will be key to this the next six months as the “re-opening” unfolds. High inflation might be temporary as the economy adjusts to the new supply-and-demand equilibrium.

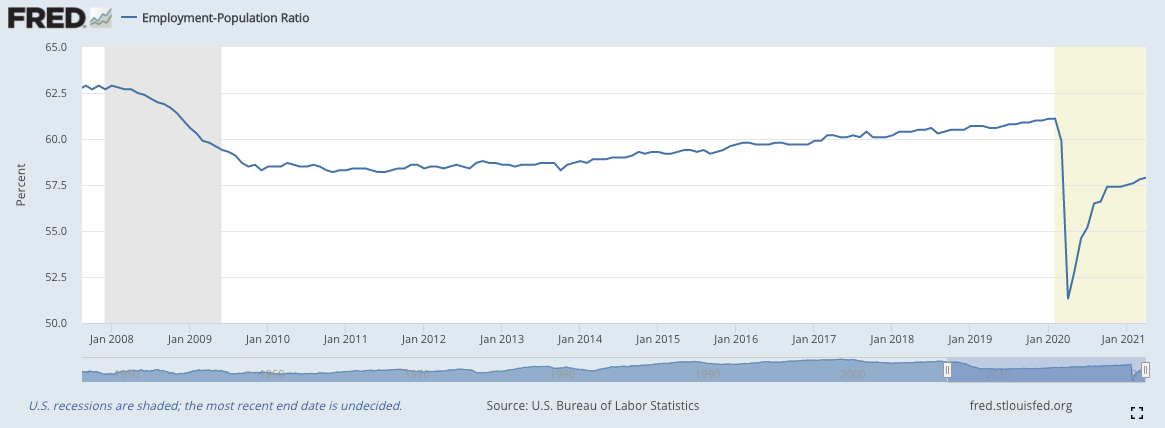

We are closely watching the employment ratio in order to gauge the speed at which individuals get back to work. The current trend and the post-2008 trend suggest that employment levels go down in a flash but take years to recover.

"Between February and April 2020, 4.2 million women dropped out of the labor force, in large part due to an unexpected caregiving burden. Nearly 2 million have not yet returned," Treasury Secretary Janet Yellen by Leticia Miranda and Caitlin Fichtel for NBC

Another element fuelling the rise in costs are shipping rates. These have exploded as sea freight has a hard time adjusting itself to the distorted global demand.

“This is uncharted territory in terms of carrier profits -- in terms of freight rates, in terms of just the level of disruption that the supply chain is seeing, […] It's unprecedented in terms of the chaos that we're seeing right now." Simon Heaney by Aurora Almendral for Nikkei Asia

2/ The Federal Reserve’s messages have been relatively more hawkish in the last weeks. Suggesting that a taper (increase in rates) might happen earlier than expected as the economy is recovering relatively fast.

“A "number" of Fed officials appeared ready to consider changes to monetary policy based on a continued strong economic recovery, according to minutes of the U.S. central bank's April meeting” by Howard Schneider and Ann Saphir for Reuters

BENCHMARK’S TAKE

Inflation and taper talks will continue to cloud the skies as long as global shipping constrain global supply chains and unemployment rates remain pressured

- Shipping constraints might start to smoothen by the start of the summer as the temporary disequilibrium gets resolved

- However, unemployment might take longer to normalise, potentially opening the door to sustained inflation

We believe these will create volatile times for equities:

- The fear of a rate-rise could continue to pressure (still richly valued) high growth names

- Short duration stocks (the ones with earnings “today” rather than “tomorrow”) such as the companies forming the Dow Jones index should continue to fare well given the massive consumer demand

- Banking stocks could continue to benefit from rising yields. On top of this, banks benefiting from volatility through their trading activities should be able to outperform the market in this setting (e.g. Goldman Sachs)

- More reasonably priced technology names should be able to fare higher, boosted by strong earnings. Especially high-growth European and Asian equities which are already profitable and still growing at a fast rate

Disclaimer

Please note that this article does not constitute investment advice in any form. This article is not a research report and is not intended to serve as the basis for any investment decision. All investments involve risk and the past performance of a security or financial product does not guarantee future returns. Investors have to conduct their own research before conducting any transaction. There is always the risk of losing parts or all of your money when you invest in securities or other financial products.

Credits